By Kamil A. Oumer

Development Bank of Ethiopia (DBE) is the only development bank for the 100 million and plus people in Ethiopia. For the last one century, the bank has been operating development financing through different monikers. After it was re-established as the Development Bank of Ethiopia in 2003, it has been empowered to provide development finance at the lowest possible rate while ensuring its sustainability. Hence, by mobilizing fund from domestic and foreign sources, it has been providing loans, lease financing, export guarantee, etc worth of billions of Ethiopian birr. The bank particularly focuses on government priority areas like commercial agriculture, strengthening small and medium enterprises (SME), agro-processing and manufacturing. The bank, however, has no interest free financial services to date. The author of this opinion piece argues that the DBE should open interest-free finance (IFF) window services for inclusive development financing.

Inclusive growth has been taken as the first of the “African aspirations” for the Agenda 2063. Agenda 2063 stipulated that the Africa we want aspires “a prosperous Africa based on inclusive growth and sustainable development.” Five of the seventeen Sustainable Development Goals (SDGs) (goals 4, 8, 9, 11, and 16) also expressly call for inclusivity. The remaining goals also implicitly address the inclusivity agenda. Therefore, inclusive development by itself is a development objective. Development in the 21st century, however, is unthinkable out of inclusive financing schemes.

The World Bank Group’s Global Financial Development Report (2019) indicates that only 34.8% of adults above 15 years have accounts in formal financial institutions in Ethiopia. Thus, more than 66% of the adult population is unbanked. A number of research works show that inaccessibility of IFF service is one of the Predicaments for financial inclusion in the country. The National Bank of Ethiopia also acknowledged that interest free finance helps promote financial inclusion in the country. The first interest free banking directive, Directives Number SBB/51/2011, reiterated that “there has been increasingly strong public demand for interest free banking” in the country. The Ethiopian National Financial Inclusion Strategy (2014-20) also averred that IFF can promote financial inclusion in Ethiopia (NBE, 2017). Further, the “(1st Replacement) Directive to License and Authorise Interest-Free Banking Business Number SBB/72/2019” underscored that “interest free banking business has to be promoted for greater financial inclusion.”

Taking advantage of the “increasingly strong public demand” and relatively favourable regulatory environment, a number of commercial banks have joined the interest-free finance industry since 2013. So far, six conventional banks have opened “full-fledged IFB branches” while additional four banks are providing window services. Two full-fledged IFBs have also already secured operational license in the current fiscal year. A data from the National Bank of Ethiopia shows that, as of September 30, 2020, over 66.3 billion birr has been mobilised through interest-free fund mobilizations schemes and 13.529 billion birr has been disbursed through IFF financing schemes. Thus, though inchoate, commercial IFF is progressing in Ethiopia. While commercial banks are availing the market for IFF, the only development bank in Ethiopia, DBE, has no IFF service to date.

Development Bank of Ethiopia, as a policy bank, is empowered to finance projects with potential impact on the overall economic development endeavour of the nation. The mission statement of the bank stipulates that it is established to:

Promote the national development agenda through development finance and close technical support to viable projects from the priority areas of the government by mobilizing funds from domestic and foreign sources while ensuring its sustainability.

The DBE finances both private and government projects so long as they are believed to have developmental impact. It Provides capital goods lease financing, finance projects in the agriculture, manufacturing, mining & energy, financial service, and personal needs of its staffs. The bank has been financing a number of projects owned by the public sector and private investors of domestic and foreign origin. It also manges funds like the youth employment creation fund released by the government in 2018, the Rural Financial Intermediation Programme (RUFIP) fund, etc. Further, it has been providing entrepreneurial and technical supports for SME and new start-ups.

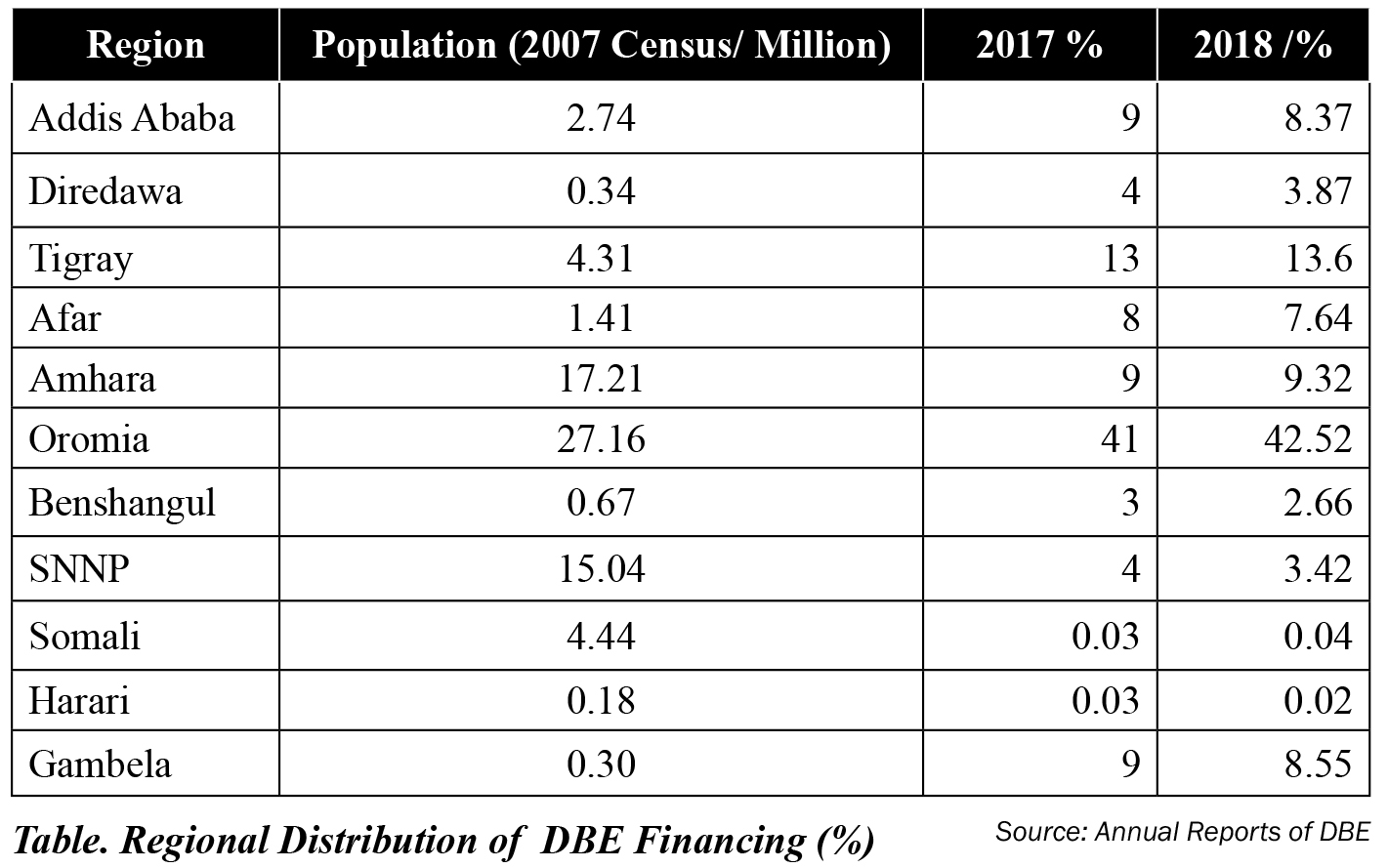

To ensure fair distribution of wealth, the bank tried to finance projects in all regional states. Following rumours in the public, it disclosed the regional distribution of its operation for the years 2017 and 2018.

Table. Regional Distribution of DBE Financing (%)

At the end of June 2019, the bank has a total asset of 83.39, paid-up capital of 7.5, loans and advances of 40.24 and customer deposit of 1.11 billion birr. It has 116 branches all over the country. The bank reported 1.87 billion and 1.670 billion birr in los for the years 2018 and 2019. In all its financing endeavours, however, DBE has no IFF schemes.

As the only development finance provider and a state owned bank, development bank of Ethiopia need to re-consider the hitherto operation and work to provide interest-free development financing schemes. Providing IFF services has already been recognized as one factor for promoting financial inclusion in Ethiopia. Failure to provide IFF services, therefore, widens financial exclusion in the country. Specifically in development financing, the failure of the sole development bank which is a state owned policy bank to provide IFF services bedevils the efforts of the country to boost financial inclusion. Introducing interest-free finance also help the bank to mobilize more fund from both domestic and foreign sources. The bank has the mandate to accept time deposit and providing all banking services for its customers. Over the past eight years, as already mentioned, commercial banks managed to mobilize over 66.3 billion birr through IFB schemes from domestic sources. This shows that the bank can mobilize its own share from the interest-free financial industry.

It is also important to note that IFF principles are more consonant with development banking than commercial banking. Adjusting capital lease financing in-to Murabaha financing, for example, requires a little more than a political will. The more than eight years of IFB experience in Ethiopia also makes predicaments in terms of knowhow and human resource less challenging. Therefore, it is high time for the Development Bank of Ethiopia to join the IFB industry.

The writer can be reached via kamillaw2009@gmail.com

{kind=link}